We’ve all heard the perpetual adage, but why exactly is property considered a long-term investment?

Acquisition & Disposal Costs

Purchasing a property carries a number of additional costs including but not limited to: transfer duty, attorneys fees, and bond registration / bond initiation fees. These costs are relative to the purchase price, i.e. the higher the purchase price the higher the costs. On a property of R1,000,000 for example, the total cost could amount to R55,000, or 5% of the purchase price. On a R10,000,000 property this cost could increase to as much as R1,100,000, or 11% of the purchase price.

Selling a property incurs further costs such as: estate agent commission (usually around 5%), compliance certificates (electrical, gas, SPLUMA, wood borer) and Capital Gains Tax on profits. Subsequently, when buying an investment property, you will have to wait for it to appreciate in value equivalent to these costs in order to break even:

Purchase price R1,000,000

Acquisition costs R55,000

Disposal costs R60,000

If we assume a value increase of 5% per annum, one would need to wait over two years to break even (R1,115,000). This period increases to three years on a property of R10,000,000, without even considering the effects of Capital Gains Tax.

Compound Interest

This is essentially ‘interest on interest’, and holds that provided your property increases in value over time, you will have the benefit of accelerated capital growth. For example: a R1,000,000 property with a 5% annual compounded growth rate will be worth R1,628,895 after 10 years, but after 20 years the property will be worth R2,653,298. Therefore in the first decade the property increased in value by R628,895, but in the second decade it increased by R1,024,403 because interest was being earned on the gains made from the first decade.

Bond Financing

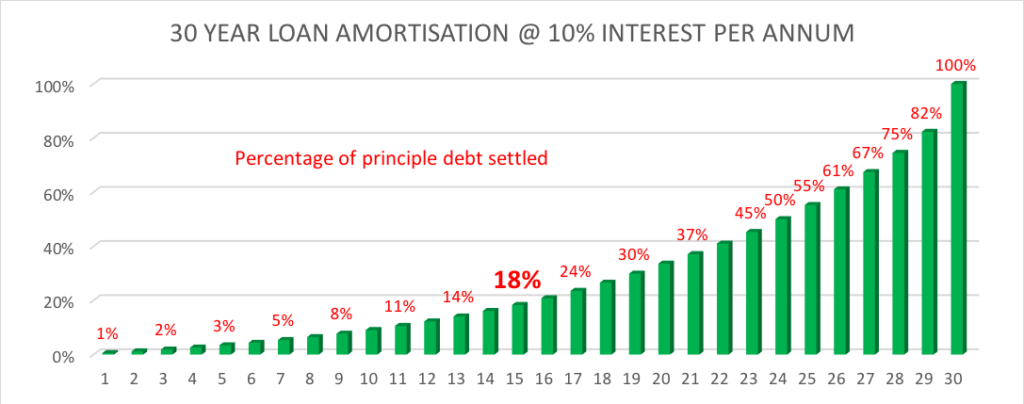

Financial institutions charge interest on loans, which is collected together with the principle loan amount over a period of time until the principle amount is settled in full. The interest payment amounts are based on the balance of the principle amount. This means that the higher the principle amount, the higher the interest charge. Subsequently the borrower pays maximum interest at the start date of a loan, and decreasing interest instalments as the principle amount is reduced over time.

The following graphs illustrate the effects of interest over time:

It’s interesting to note how little the principle debt is diminished in the initial years of each loan. The mid-point of a loan period does not translate to a 50% reduction in the principle debt as one would expect, but rather the principle amounts are only settled by 38%, 27% and 18% halfway through the 10 year; 20 year and 30 year loan periods respectively.

Notwithstanding the above, 90% of the world’s millionaires create wealth through property investment, showcasing the success of a long-term mindset that should be applied to all portfolios, no matter how big or small.